Loans

Stafford Loan Program

The Federal Direct Subsidized and Unsubsidized Stafford loans are federal student loans offered by the U.S. Department of Education for eligible students to help cover the cost of higher education.

Subsidized/Unsubsidized Stafford Loans

All Stafford Loans:

- Enter repayment six months after graduation or when you cease attending a place of higher education

- Are set at a fixed-interest rate

- Have an origination fee deducted from the loan funds by the Department of Education

- For more information on the current interest rates and origination fees, see studentaid.ed.gov

Key Differences:

Subsidized Stafford loans:

- Are available to students with financial need

- The Department of Education pays the interest on subsidized loans while the student is enrolled in school at least half-time.

Unsubsidized Stafford loans:

- Are available to Students regardless of financial need

- Interest begins accruing at the point the loan is disbursed onto your student account (this is typically ten days before the semester begins)

*Financial Need is defined as the Cost of Attendance minus all Financial Aid.

| Annual Loan Limits | ||||

|---|---|---|---|---|

| Year in School | Dependent Student Total | Independent Student Total | Maximum Subsidized Portion (Based on Financial Need) | Additional Unsubsidized if Parent PLUS loan is denied |

| Freshman | $5,500 | $9,500 | $3,500 | $4,000 |

| Sophomore | $6,500 | $10,500 | $4,500 | $4,000 |

| Junior and Senior | $7,500 | $12,500 | $5,500 | $5,000 |

Loans cannot exceed the cost of attendance less other financial aid.

| Maximum total debt from Stafford loans when you graduate (Aggregate loan limits) | ||

|---|---|---|

| Dependent Student Total | Independent Student Total* | Maximum Subsidized Portion (Based on Financial Need) |

| $31,000 | $57,500 | $23,000 |

*And Dependent Students who's parents cannot borrow from the Plus loan program

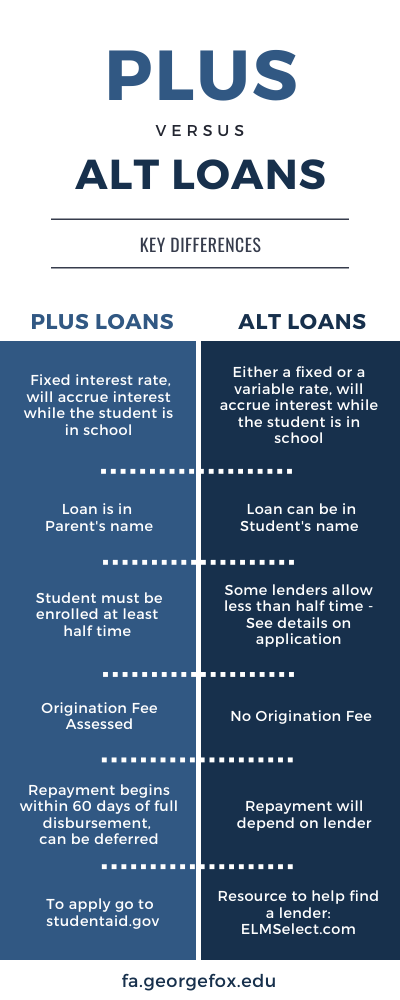

Parent PLUS Loans

|

|

Compare Plus and |

Parent PLUS loans are federal loans provided by the U.S. Department of Education that parents of dependent undergraduate students can use to help pay education expenses.

Parent Plus loans:

- Are in the parent's name

- Are approved based on a soft credit check of the parent

- Have a fixed-interest rate

- Have an origination fee deducted from the loan funds by the Department of Education

- Repayment Information:

- Begins within 60 days of disbursement of loan

- Can be deferred while student is enrolled at least half-time by request in the application

- To learn more about Parent PLUS Loan repayment, visit Direct Parent PLUS Loans.

*Plus loans applications become available in May for the following academic year.

How Do I Apply?

- The application can be found at studentaid.gov

- Parents must log in with their FSA username and password

- Parents will receive approval or denial right away

- The school will be notified in 24 Hours

- Applications are aid year specific and must be completed each year

- The loan amount can be specified during the application process as one of the following:

- Maximum amount (the student’s cost of attendance minus all other financial aid)

- Specific amount (the parent chooses the loan amount)

- Unknown amount (contact Financial Aid Counselor)

- Parent must complete PLUS Master Promissory at studentaid.ed.gov

Example Parent Plus loan Application: https://studentaid.gov/app/plusAppHtml.action

What If I Am Denied?

In some cases, when a parent is denied, they may still be able to receive a PLUS loan by:

- Obtaining an endorser who does not have an adverse credit history.

- An endorser code should be provided at the time you complete the application.

- Parents need to complete a PLUS Master Promissory Note for each endorsed loan.

- Parents will also need to complete PLUS Counseling before disbursements of the loan can be made.

- Appealing the credit decision by documenting to the Department of Education's satisfaction extenuating circumstances relating to their adverse credit history.

- Parents will need to complete PLUS Counseling before disbursements of the loan can be made.

Not seeking an endorser or appealing?

The student may be eligible for additional unsubsidized loans in the following amounts:

- Freshman and Sophomore: $4,000

- Junior and Senior: $5,000

Alternative Loans

Alternative loans are private loans that are not part of the federal financial aid program.

Private loans:

- Interest rates and fees vary greatly and may depend on the borrower’s credit-worthiness

- Have both fixed and variable-interest rate options

- Generally, students are required to have a cosigner

- Loan amounts cannot exceed the cost of attendance minus all other financial aid

- Can be in the student or parent’s name

- Have no loan origination fee

- Repayment deferment options may vary

- Interest begins accruing at the point the loan is disbursed onto your student account (this is typically ten days before semester begins)

Where do I find a Private Loan?

These resources will help you make an informed decision about the most appropriate loan for you

- Check with your personal bank or credit union

- Try ELMSelect to view and compare lenders that have provided private loans to George Fox students in the past.

- Please note that you are not required to select a lender on this list.

- You can also visit ConsumerAffairs.com for helpful tips on how to choose a student loan lender.

* Your Financial Aid Counselor can not recommend any private lender but can help you understand your options

Federal Perkins Loan Program

The Federal Perkins Loan is a need-based loan with a fixed interest rate (5%). It is offered to full time traditional undergraduate students with high financial need, and generally awarded to Freshmen. George Fox University generally limits the annual award level of Perkins loans to $1000. Repayment of the Perkins loan begins 9 months after the student graduates or ceases to be enrolled at least 1/2 time. Funding for the Federal Perkins Loan program is limited. Students who borrow from the Federal Perkins Loan program are borrowing the funds from George Fox University.

NOTE: The Federal Perkins Loan Program expired October 1, 2017.